Intel is no longer just a CPU company. It has transformed into a critical asset for U.S. national security. If you’re looking at the recent stock chart, you’ll see a dramatic “V-shaped” recovery. Let’s dive into why the market is betting big on Intel again.

1. The Chart: A Powerful Rebound

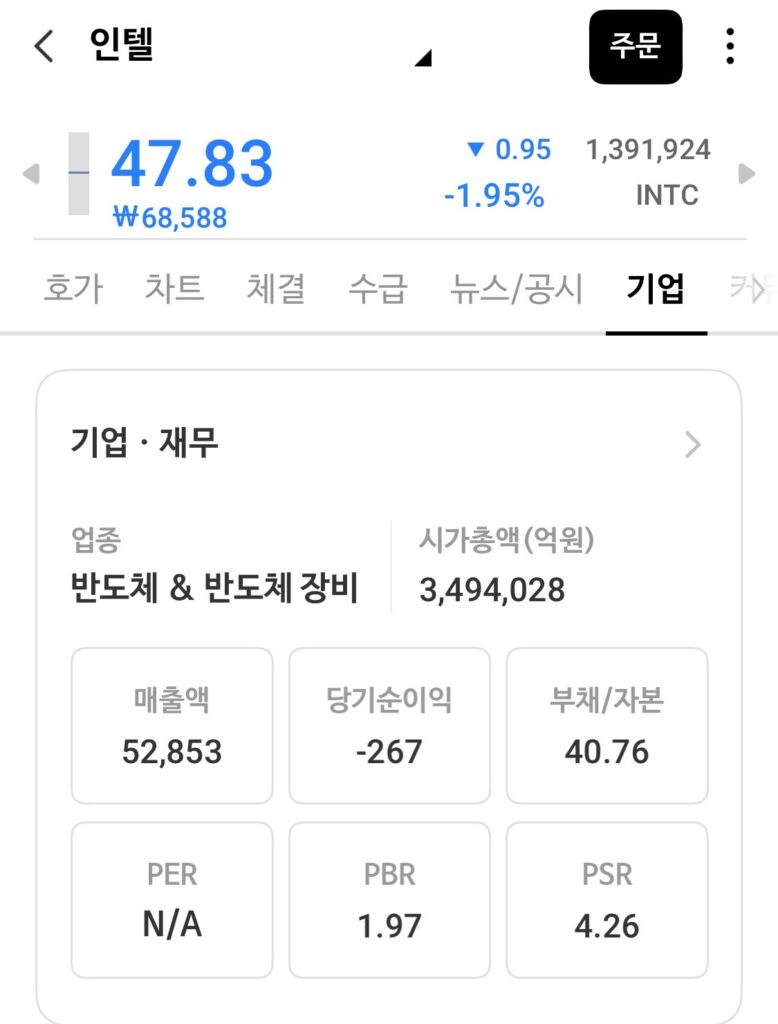

Looking at the monthly chart, Intel hit a rock bottom of $17.66 in April 2025. Fast forward to today, the stock is trading around $47.83, a staggering 170%+ increase.

- The Takeaway: Strong trading volume at the bottom confirms that institutional “smart money” has moved back in, signaling a long-term trend reversal.

2. Key Financials at a Glance

- Market Cap: Approx. $243.6 Billion.

- PBR (Price to Book Ratio): 1.97x – The stock is no longer “dirt cheap” but is still reasonably valued considering its massive physical assets (fabs) in the U.S.

- Profitability: While currently showing a net loss due to massive R&D and factory construction, revenue growth in the AI and Foundry sectors is accelerating.

3. Why Intel is Winning: The “Big Three” Comparison

To understand Intel’s edge, we must compare it to its two main rivals: TSMC (Taiwan) and Samsung (South Korea).

| Category | TSMC | Samsung | Intel |

| Position | The Undisputed Leader | The Tech Challenger | The American Champion |

| Core Strength | Best Yield & Reliability | Memory + Logic Integration | Geopolitical Safety |

| Main Risk | China-Taiwan Tensions | Yield Stability Issues | Execution of 18A Node |

4. Intel’s Unfair Advantages

1) The “National Foundry” Status In August 2025, the U.S. government acquired a 10% stake in Intel. This effectively turned Intel into a “Government-backed” entity. For global investors, this means the U.S. government will not let Intel fail, providing a massive safety net.

2) Geopolitical “Safe Haven” As tensions rise in Asia, Big Tech giants like Apple, Nvidia, and Microsoft are desperate for a “Plan B.” Intel offers the most advanced manufacturing sites on U.S. soil. In a world of supply chain uncertainty, “Made in USA” is a premium feature.

3) 18A (1.8nm) Leapfrog Intel is skipping generations to catch up. Their upcoming 1.8nm (18A) process is designed to rival or even beat TSMC’s best technology. If Intel proves it can mass-produce these chips with high quality, the floodgates of orders will open.

Summary for Investors

Intel has shifted from a struggling legacy giant to a strategic powerhouse. Backed by the U.S. government and fueled by the AI revolution, it is positioned to be the primary alternative to TSMC. For those watching the “Silicon Shield” move to the West, Intel is the ticker to follow.